What Requirements Do Service Providers Owe To Their Client

Executive Summary

CFP® professionals – similar any professional – are expected to give advice in the best interests of their clients. Both every bit a authentication of professionalism, and only because it's practiced business to do so. Yet in exercise, information technology'south not enough to just say that CFP® professionals are fiduciaries; professional adherence requires setting forth clear Standards of Conduct well-nigh how, exactly, CFP® professionals are expected to deliver their services in a fiduciary manner, so CFP Lath can determine when a CFP® professional is not meeting their obligations and may demand to be disciplined… or, at worst, accept their CFP® marks suspended or revoked.

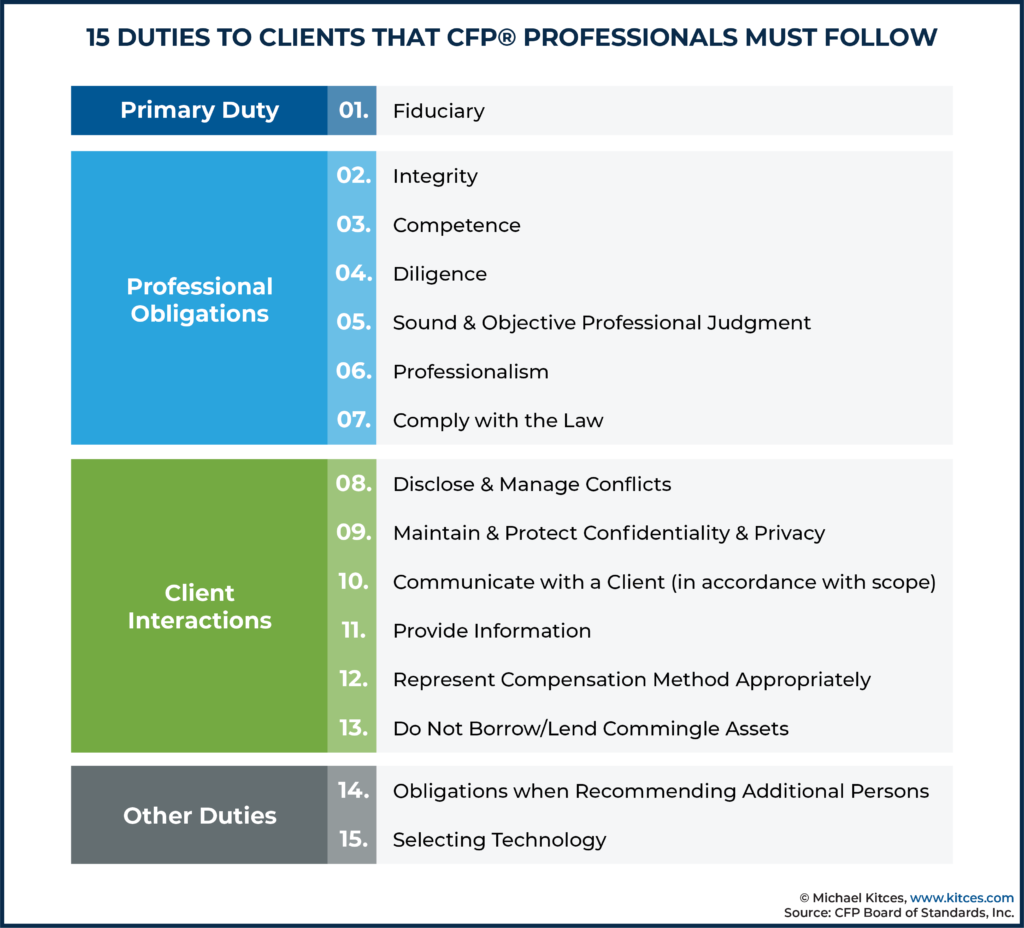

To provide articulate guidance, CFP Board'due south new Lawmaking of Ideals and Standards of Conduct ("Lawmaking and Standards") delineate a series of xv Duties To Clients that CFP® professionals must adhere to, from the Fiduciary Duty to Clients itself, to an obligation for providing central information and relevant disclosures of Material Conflicts of Involvement, confidentiality obligations, the duty to uphold cadre professional principles including Integrity, Competence, and Diligence, as well as entirely new Duties regarding the selection of external professionals (to which the CFP® professional may refer clients) and even the selection of technology itself.

In improver, CFP Lath's new Code and Standards also institute new guidance in previously controversial areas, specially with respect to how CFP® professionals disclose their bounty, and the use of compensation disclosures equally a marketing term (e.m., the "Fee-Only" label)… not to induce CFP® professionals towards any mode of bounty in particular, merely simply to ensure that whatsoever bounty methodology the CFP® professional person chooses, that they are accurate in how they describe their prospective compensation to their Clients.

In the end, the 15 Duties Owed To Clients past CFP® professionals are not meant to impose substantial new obligations on CFP® professionals – and in reality, are unremarkably followed and generally recognized as best practices anyway. Still, though, by enumerating the 15 Duties as role of the Lawmaking and Standards itself, CFP Board both provides boosted guidance to CFP® professionals on what they are expected to do equally a affair of not just "all-time" just standard practices… and besides establishes the grounds by which CFP® professionals may be disciplined for failing to encounter the minimum standard of their professional duties!

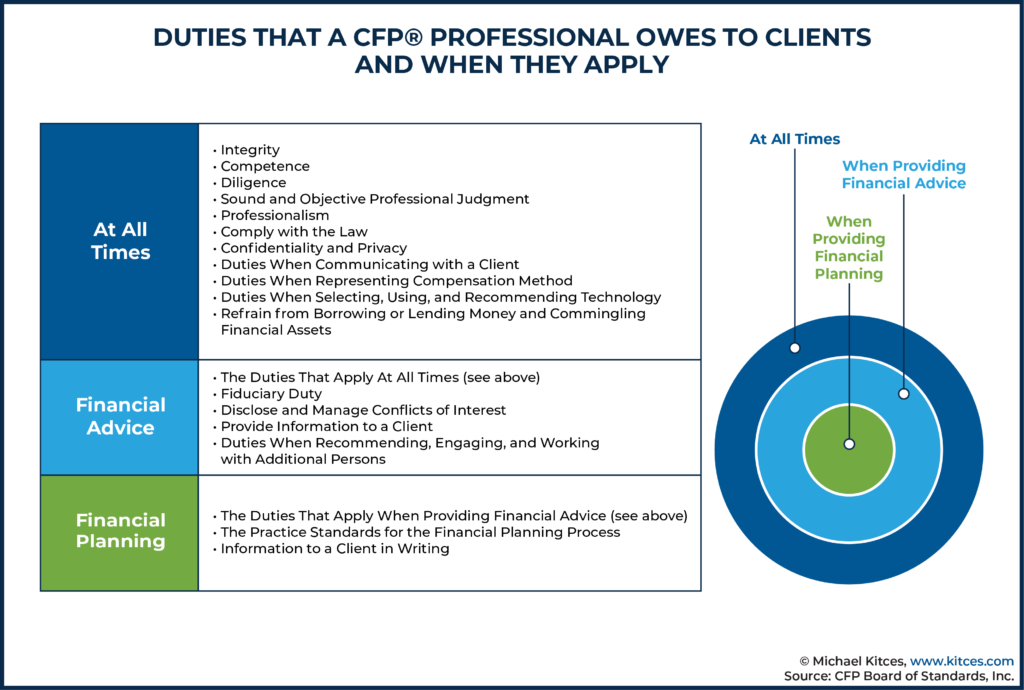

The 15 Duties To Clients That All CFP® Professionals Must Follow

CFP Lath's new Code and Standards , which first took effect in Oct of 2019 and were enforced as of June 30th of 2020, imposed for the starting time time a new "fiduciary at all times" Standard while providing financial advice to clients on CFP® professionals. As while in the past, CFP® professionals were 'only' required to be fiduciaries when providing Financial Planning or material elements of Financial Planning (but non merely for merely 'existence' a CFP® professional providing advice and recommendations to clients), the new rules require CFP® professionals to adhere to a fiduciary duty any time they provide Financial Advice to clients (regardless of whether full Fiscal Planning was required or non).

Yet, CFP Lath'south Code and Standards obligate CFP® professionals to more than 'merely' a fiduciary obligation to act in the best interests of their clients. As a fiduciary obligation alone guides CFP® professionals on the ultimate Standard to which they will exist held accountable… but non necessarily to the specific duties that CFP® professionals are expected to fulfill in order to meet that obligation.

Accordingly, CFP Board'due south new Code and Standards include a series of 15 "Duties Owed To Clients" that all CFP® professionals must adhere to, regardless of whether providing Financial Planning or non-Financial-Planning Fiscal Advice, in society to fully meet their obligations to clients who take engaged them for professional person services.

xv Duties Owed To Clients

- Fiduciary Duty to Clients

- Disclose and Manage Conflicts of Interest

- Providing Information to Clients (and Prospects)

- Communicating (Clearly) with Clients

- Integrity

- Competence

- Diligence

- Sound and Objective Professional person Judgment

- Professionalism

- Confidentiality and Privacy

- Properly Representing Compensation Method

- Due Diligence Duties When Recommending, Engaging, and Working with Boosted Persons

- Comply with the Law

- Duties When Selecting, Using, and Recommending Technology

- Not Borrowing From, Lending To, or Commingling Financial Assets with Clients

Failure to follow CFP Board's 15 Duties Owed To Clients (or the Duties owed to Business firm and Subordinates, or the Reporting and other Duties owed to CFP Board itself) will consequence in potential disciplinary activeness, which may include Individual Censure, a Public Censure, suspension, or in the extreme, revocation of the CFP® marks. In addition, failure to adhere to CFP Board's Practise Standards when delivering financial planning can also trigger disciplinary action.

ane) Fiduciary Duty To Clients

The anchor of the new Code and Standards – as embodied by literally being the first enumerated Duty to clients – is the obligation to act as a fiduciary acting in the best interests of the Client at all times when providing Financial Communication.

More specifically, the new Fiduciary obligation for CFP® professionals entails 3 underlying Duties that the CFP® professional person must fulfill:

- Duty of Loyalty. The Duty of Loyalty specifically requires that the CFP® professional must:

- Place the interests of the Client above the interests of the CFP® professional person and the CFP® professional'south Firm;

- Avoid Conflicts of Interest, or fully disclose Fabric Conflicts of Involvement to the Customer, obtain the Customer's informed consent, and properly manage the conflict; and

- Deed without regard to the financial or other interests of the CFP® professional, the CFP® professional's Firm, or whatsoever individual or entity other than the Customer, which means that a CFP® professional interim under a Conflict of Interest continues to take a duty to deed in the all-time interests of the Client and identify the Client'due south interests above the CFP® professional'due south.

- Duty of Intendance. CFP Board's Duty of Care requires that the CFP® professional must:

Act with the care, skill, prudence, and diligence that a prudent professional would exercise in light of the Client'south goals, hazard tolerance, objectives, and fiscal and personal circumstances.

- Duty to Follow Client Instructions. CFP Board's Duty to Follow Customer Instructions requires that the CFP® professional person must:

Comply with all objectives, policies, restrictions, and other terms of the Engagement and all reasonable and lawful directions of the Client.

Notably, the end result of these 'sub-Duties' of the Fiduciary Duty is that CFP® professionals are not only generally expected to deed in the best interests of their clients, just they should only provide advice in areas in which they are competent to advise (i.due east., they can provide services with the care, skill, prudence, and diligence of a professional).

On the other hand, in situations where the Client themselves disregards the CFP® professional person's Best-Interests advice, and so asks the CFP® professional person to implement an action reverse to their ain advice, the CFP® professional person still is expected to and has an obligation to follow the Client'southward instructions (presuming they are otherwise reasonable and legal in the showtime place). In other words, CFP® professionals are not obligated to cease clients who pass up to accept their advice or choose a unlike grade of activeness instead.

2) Disclose And Manage Conflicts Of Interest

CFP Board defines a conflict of interest as when a CFP® professional person's "interests (including the interest of the CFP® professional person's firm) are agin to the CFP® professional'due south duties to a Client… or [when] a CFP® professional has duties to one Client that are adverse to another Customer."

To the extent that a CFP® professional faces (Material) Conflicts of Interest in providing advice to clients (and/or in how they are compensated for that advice and implementation), CFP Board'due south Code and Standards require that:

When providing Financial Advice, a CFP® professional must fill disclosure of all Textile Conflicts of Interest with the CFP® professional person's Client that could affect the professional human relationship. This obligation requires the CFP® professional person to provide the Client with sufficiently specific facts so that a reasonable Client would be able to understand the CFP® professional's Material Conflicts of Interest and the business practices that give rise to the conflicts, and give informed consent to such conflicts or pass up them.

Such disclosures do non accept to be delivered in writing (i.e., oral disclosure is permitted, as long as it is still given earlier providing Financial Advice), but are required to encompass the full scope of the CFP® professional's Engagement with a Client (and thus may go beyond the standalone required disclosures of FINRA broker-dealers and/or RIAs via Form ADV Office ii and/or Form CRS).

In addition, to the extent the CFP® professional does retain a Material (and now disclosed) Conflict of Interest, they are expected to manage the touch on of that Conflict:

A CFP® professional must adopt and follow business concern practices reasonably designed to prevent Material Conflicts of Interest from compromising the CFP® professional person'south ability to act in the Client's best interests.

In this context, "Material" is defined by CFP Board as "when a reasonable Customer or prospective Client would consider the Conflict of Interest important in making a decision".

3) Providing Information To Clients (And Prospects)

Establishing the Telescopic of an Engagement is a central requirement for whatever and every professional, as it's only by clearly defining (and often, limiting) the Scope of Engagement that the professional tin can ensure their ability to render all of their agreed-upon duties at a professional level. Later on all, if the CFP® (or any) professional commits to practise 'everything' for the Client, at some bespeak there'due south a risk that the professional operates outside their primary domain of skill (putting them in breach of their Duty of Care to clients).

In the context of the new CFP Lath Code and Standards, the get-go Duty of CFP® professionals when it comes to defining the Scope of Engagement is only an obligation to provide to clients all the data they would need to know in order to make a decision almost a prospective Engagement, including providing data with respect to:

- The CFP® professional's Services and Products (description of services and/or products to be provided);

- How the Customer Pays (for any products and services rendered);

- How the CFP® professional (and Related Parties) are compensated;

- Public Subject field or Bankruptcy (including relevant government agencies or regulatory authorities that may report on disciplinary matters);

- Material Conflicts of Interest (as discussed earlier);

- Privacy Policy (regarding "Written Notice Regarding Non-Public Personal Information");

- Referral Compensation Arrangements (i.e., revenue-sharing and other referral compensation agreements, equally discussed later); and

- Whatever Other Fabric Information.

In the case of broad-based "Fiscal Advice" (that does not crave the total Financial Planning Exercise Standards), the CFP® professional must provide the information to the Customer either prior to or at the time of Date, only may provide the information orally (though the CFP® professional person is still expected to document that the data was in fact provided in a timely manner).

However, when a full-fledged Financial Planning Engagement occurs (where the Fiscal Planning Practice Standards apply), the CFP® professional must not only provide the aforementioned information in written format (except for Fabric Conflicts of Interest that may remain orally disclosed), but is too expected to formalize the "terms of the Appointment" between the Client and the CFP® professional person (or their firm), including the Telescopic of Engagement and any limitations, the menstruum(s) during which the services will be provided, and the Customer's responsibilities.

Formal documentation of the Telescopic of Engagement is particularly important in the context of a Financial Planning Engagement, as by default, a CFP® professional is presumed to exist responsible for implementing, monitoring, and updating the Financial Planning recommendation(s) as well, unless those duties are specifically excluded from the Scope of Engagement.

Notably, the Duty to Provide Information to Clients also includes an ongoing obligation to provide updated information when there is a Material modify or update to the information required to exist provided to the Customer (the Code and Standards does not specify a precise number of days). Textile changes or updates to the counselor's public disciplinary history or bankruptcy data must be disclosed to the Client within 90 days.

4) Communicating (Clearly) With Clients

Although common amid CFP® professionals simply every bit a expert concern do, the new Code and Standards explicitly require that CFP® professionals communicate clearly with clients.

Specifically, the Standard requires that CFP® professionals provide accurate information, communicate in accordance with the Telescopic of the Client Engagement (i.east., provide timely advice or responses to questions/topics in which the CFP® professional is engaged), and reply to reasonable client requests in a fashion and format that the Client reasonably may be expected to empathise.

While in practice, the Articulate-Communication Duty should exist fairly straightforward for CFP® professionals to comply with, it is both an important reminder virtually clearly defining the Scope of Engagement (if simply to brand clear what the CFP® professional is and is not expected to communicate about in a timely manner), and that communication must occur in a style and format that clients can understand. (Which, notably, ways CFP® professionals would exist expected to brand communication accommodations for clients who may be hearing or especially visually dumb.)

5) Integrity

In the prior version of CFP Board'due south Lawmaking of Ideals and Professional Responsibility, CFP Board espoused a serial of 7 Principles – Integrity, Objectivity, Competence, Fairness, Confidentiality, Professionalism, and Diligence – which, in the new version, are incorporated (in a restated manner) into the Lawmaking of Ethics and also codified in the new Lawmaking and Standards as a formal reflection of the exact duties expected of a CFP® professional to their Customer.

When it comes to the principle of integrity, the new Standards specifically require that:

- A CFP® professional must perform Professional Services with honesty and candor, which may not be subordinated to personal gain or advantage.

- A CFP® professional may non, straight or indirectly, in the conduct of Professional Services:

- Employ any device, scheme, or bamboozlement to defraud;

- Make whatever untrue statement of a fabric fact or omit to state a material fact necessary in society to brand the statements made, in the low-cal of the circumstances under which they were fabricated, non misleading; or;

- Engage in any act, exercise, or grade of business organization which operates or would operate as a fraud or cant upon whatever person.

In essence, the Integrity Standard means that the CFP® professional must be truthful and candid with clients, and not appoint in whatsoever actions that are misleading or make statements that are untrue. Notably, as CFP Board acknowledges, "Allowance may be made for innocent error and legitimate differences of opinion". Nevertheless, "integrity cannot co-exist with cant or subordination of principle."

6) Competence

I of the cadre tenets of Professionalism and a Fiduciary Duty (under the Duty of Care) is to only provide communication in areas in which the professional is competent to provide advice in the first place.

This obligation for Competency is another that was previously embodied as i of the vii Principles of the prior Lawmaking of Ethics and Professional person Responsibility and has been expanded as one of the 15 Duties to Clients under the new Lawmaking and Standards.

Under the new rules, the Competency Standard means providing professional services "with relevant noesis and skill to apply that knowledge".

A key aspect of the Competency Standard is that when a CFP® professional person does non accept competency in a detail domain (eastward.g., whether information technology pertains to in-depth tax planning, a specialized domain like divorce planning, or a technical subject area affair the CFP® professional has express noesis and experience with, such as student loan planning), the CFP® professional is expected to:

- Proceeds competency;

- Obtain assist from a competent professional;

- Limit the Scope of Engagement to exclude the topic;

- Terminate the Engagement for being unable to fulfill the Engagement competently; or

- Refer the Customer out to a competent professional person.

Notably, in the event that the CFP® professional is not competent plenty to provide services on a sure topic, the CFP® professional person is expected to clearly describe to the Customer (and define in the Telescopic of Engagement) the services that volition not be provided.

7) Diligence

Another of the Principles of the prior Code of Ideals and Professional Responsibility was Diligence, and the expectation that a CFP® professional volition provide their services diligently.

The Oxford Dictionary defines existence diligent as "having or showing care and conscientiousness in one'southward work or duties". And in fact, prior Kitces Research finds that fiscal planners as a whole tend to be well above average in their Conscientiousness (one of the 'Large Five' personality traits).

Nonetheless, as a professional Standard of Bear, CFP® professionals are expected to provide their Professional Services diligently, including responding to reasonable Client inquiries, in a timely and thorough manner.

8) Sound And Objective Professional Judgment

Going hand-in-hand with the fiduciary obligation of a Duty of Loyalty to act in the Client'south best interests is a responsibility to render professional services objectively, which was already role of the prior Principles-based Code of Ethics and is now embodied in the new Code and Standards as a Duty to return services to the Client with Sound and Objective Professional Judgment.

Notably, the Objectivity Duty is not only a matter of trying to engage in sound judgment, but also that the CFP® professional person must not engage in any actions that could compromise their Objective Professional person Judgment. Accordingly, the CFP® professional "may not solicit or accept any gift, gratuity, entertainment, non-cash compensation, or other consideration" that reasonably could exist expected to compromise their Objectivity.

In practice, the limitations on gifts and gratuities under existing FINRA and SEC regulations would likely already bear to the obligation for CFP® professionals to maintain (and non compromise) their Objectivity. Nonetheless, the obligation under the Objectivity Duty is not merely to "adjust to other regulations regarding the non-acceptance of [big] gifts", simply that the CFP® professional has an obligation to maintain their Objectivity and not accept gifts that may compromise it (even if those gifts were non prohibited past other regulatory bodies).

ix) Professionalism

Beyond virtually all recognized professions, there is a basic expectation that professionals act like 'professionals', and the new Code and Standards are no unlike.

Accordingly, a CFP® professional is expected to "treat Clients, prospective Clients, fellow professionals, and others with dignity, courtesy, and respect".

Notably, CFP Board'southward disciplinary history and its Bearding Case Histories practice not include any incidents where "professionalism" (or lack thereof) solitary was the basis for a disciplinary activity, in function because, in the past, Professionalism was part of the Code of Ethics merely not explicitly a Standard of Conduct. It remains to be seen what level of "unprofessionalism" would constitute enough to merit disciplinary activeness under the new Code and Standards. But given that "Professionalism" is now really embodied as a specific Standard of Conduct, it leaves the door open for potential disciplinary action (at to the lowest degree a Individual Censure if non a Public Alphabetic character of Admonishment or more severe enforcement action) for unprofessionalism.

ten) Confidentiality And Privacy

Maintaining both Confidentiality about Clients themselves, and Privacy regarding their private client data, is some other staple of the standard obligations of professionals and is another area that CFP Board converted from a prior Principle nether the original Code of Ideals and Professional Responsibility, into a specific Standard of Conduct nether the new rules.

In practice, the new CFP Board Lawmaking and Standards prescribe 4 core obligations with respect to Client Confidentiality and Privacy:

- Maintain client confidentiality (and do non disclose whatever non-public personal data about prospective, current, or former clients);

- Do not utilize non-public personal information about a Client for the CFP® professional's direct or indirect benefit (regardless of whether doing so is detrimental to the Client) unless the Client consents;

- Take reasonable steps to protect the security of non-public personal client information; and

- Prefer and implement policies and procedures regarding the protection, treatment, and sharing of a Client's not-public personal information, and share those policies and procedures in written format (e.g., equally a Privacy Policy) with new clients at the time of Engagement and not less oftentimes than annually thereafter.

In this context, it'southward important to recognize that protecting the security of individual client information includes information stored both physically or electronically and, equally such, 'cybersecurity' of client information is also effectively a requirement under CFP Board's Lawmaking and Standards, in improver to other regulators like the SEC and FINRA. And that any the advisor's cybersecurity policies and procedures are, they're expected to be shared annually with clients (upfront and annually thereafter).

On the other hand, CFP Board guidance does indicate that firms already compliant with Reg S-P (which by and large includes both broker-dealers and RIAs) or "substantially equivalent federal or state laws or rules" will be deemed to have complied with CFP Lath's policies-and-procedures requirement (and the almanac Reg S-P privacy find will satisfy the annual customer notification procedure). Appropriately, CFP Board's Confidentiality obligations for privacy policies will by and large only apply to those providing Financial Planning or Financial Communication services in unregulated roles (where Reg S-P or similar Federal or land privacy notice rules aren't applicable). Though either way, such rules merely excuse (or already cross-utilise) towards the CFP® certificant'south written-privacy-notification obligation; the rest of the Confidentiality Duty continues to apply regardless.

However, information technology's important to annotation that it is yet appropriate to employ non-public, private client information under CFP Board rules for ordinary business purposes, including:

- With the client'due south consent, so long as the client has not withdrawn the consent;

- To a CFP® professional's House or other persons with whom the CFP® professional is providing services to or for the client, when necessary to perform those services;

- Equally necessary to provide information to the CFP® professional person's attorneys, accountants, and auditors; and

- To a person acting in a representative capacity on behalf of the client.

In other words, the Confidentiality rules are not meant to restrict a CFP® professional's power to carry their 'normal' business concern, including working with other exterior professionals in joint work with clients, and those who are properly acting as representatives on behalf of the Customer. As long equally the CFP® professional can properly affirm those outside individuals are properly engaged with or on behalf of the Customer.

In add-on, private customer information may even so be shared when proper for legal or enforcement purposes, including:

- To law enforcement government apropos suspected unlawful activities, to the extent permitted by the constabulary;

- Equally required to comply with federal, state, or local constabulary;

- Equally required to comply with a properly authorized civil, criminal, or regulatory investigation or test, or subpoena or summons, past a governmental say-so;

- As necessary to defend against allegations of wrongdoing fabricated by a governmental authority;

- As necessary to present a civil merits confronting, or defend against a civil claim raised by, a customer;

- As required to comply with a asking from CFP Lath apropos an investigation or arbitrament; and

- As necessary to provide information to professional organizations that are assessing the CFP® professional'southward compliance with professional person standards.

In other words, while client Confidentiality and Privacy should be maintained, CFP® professionals are still expected to work productively with regulators and police force enforcement, whether regarding a bona fide investigation pertaining to the Client themselves (eastward.yard., in the instance of suspected unlawful activities), or an investigation against the advisor pertaining to a particular customer.

In add-on, the CFP® professional is too expected and required to comply with CFP Lath'south own investigation and arbitrament process, for which client Confidentiality and Privacy is not a valid alibi to refuse to provide information (at least under CFP Lath confidentiality rules, though CFP® professionals must still exist certain to comply with FINRA, SEC, or other regulatory guidelines that may utilize to them, even in the example of a CFP Board investigation and request for data).

xi) Properly Representing Compensation Method

As noted earlier, one of the fundamental requirements of beingness a fiduciary is to avoid Conflicts of Interest, and where such Conflicts are unavoidable, to at least have steps to manage them, disclose them to the Client, and obtain informed consent from the Customer. Which means clients must take a clear understanding of the advisor's prospective Conflicts of Interest, including the compensation that advisors may receive that gives ascension to such Conflicts.

And in practice, the increasingly high profile of bounty descriptions (and especially the "Fee-Only" label) in recent years, combined with the rising number of disciplinary actions for improper use of those bounty labels, led CFP Lath'due south Commission on Standards to revisit and ultimately revise the rules for Compensation disclosures going forward.

At their cadre, the new Lawmaking and Standards yet require that CFP® professionals only use the "Fee-Only" label if their bounty is, in fact, only from fees and not commissions, stating that:

Fee-Only. A CFP® professional may stand for his or her or the CFP® professional's Firm'southward bounty method as "fee-but" but if:

- The CFP® professional and the CFP® professional'south Firm receive no Sales-Related Compensation; and

- Related Parties receive no Sales-Related Compensation in connection with any Professional Services the CFP® professional or the CFP® professional'due south House provides to Clients.

In turn, the new rules explicitly prohibit CFP® professionals from using "'fee-based' or whatsoever other similar term that is not fee-only… in a manner that suggests the CFP® professional or the CFP® professional person'due south business firm is fee-merely". Instead, regardless of whether the firm is utilizing a fee-based Engagement for at least a subset of accounts with clients, if the CFP® professional is not Fee-Only, they "must clearly state that either the CFP® professional or the CFP® professional's Firm earns fees and commissions, or that the CFP® professional or the CFP® professional's House are not fee-only".

Notably, in the new "Fee-But" Compensation definition, the central requirement is not that the advisor merely received compensation from a series of specified types of fees (east.grand., AUM fees, hourly or flat project fees, monthly subscription or retainer fees, etc.), only instead that the CFP® professional person does not receive any "sales-related" (i.e., commission) compensation.

In plough, Sales-Related Compensation for the purposes of Compensation disclosures is defined as:

Sales-Related Bounty. Sales-Related Bounty is more than a de minimis economical benefit, including any bonus or portion of compensation, resulting from a Client purchasing or selling Financial Assets, from a Client holding Financial Assets for purposes other than receiving Fiscal Advice, or from the referral of a Client to any person or entity other than the CFP® professional's Firm. Sales-Related Bounty includes, for case, commissions, abaft commissions, 12b-ane fees, spreads, transaction fees, revenue sharing, referral or solicitor fees, or similar consideration.

Not surprisingly, the core of the definition of "Sales-Related Compensation" is around commissions that are generated from a client purchasing or selling financial assets (east.1000., the traditional sales or transaction-related commission), or similar payments on an ongoing footing for standing to hold such assets (eastward.g., levelized commissions that continue to be paid after the original sale). As CFP Board's own definition notes, this may include (upfront) commissions, trailing commissions such as 12b-1 fees, spreads (e.g., for private bond transactions), and other transaction fees.

However, it's important to recognize that the proper employ of the "Fee-Simply" label ways not only that the CFP® professional themselves receive no "sales-related compensation", but also that no related parties receive such compensation in connection with the CFP® professional'due south services. In this context, "Related Party" and "In Connection With" are defined as:

Related Party. A person or business entity (including a trust) whose receipt of Sales-Related Bounty a reasonable CFP® professional person would view every bit straight or indirectly benefiting the CFP® professional or the CFP® professional's Firm.

In Connection with any Professional Services. Sales-Related Compensation received by a Related Party is "in connection with any Professional person Services" if information technology results, directly or indirectly, from Client transactions referred or facilitated by the CFP® professional or the CFP® professional's House.

In other words, the mere fact that a Related Party earns/generates Sales-Related Compensation (e.g., commissions) is non plenty alone to run afoul of the rules. Otherwise – especially given the Related Party rules for family members – a CFP® professional might lose their eligibility to claim "Fee-Only" status because their brother happens to exist a wellness insurance agent, or their spouse is a real estate amanuensis, or the family owns a mortgage concern… all scenarios where family members are receiving "sales-related compensation" (in their corresponding jobs/businesses).

Instead, when it comes to Related Parties, the receipt of Sales-Related Compensation merely counts when it is received "in connection with any Professional Services" that the CFP® professional person (or his/her business firm) really provides to Clients.

On the other hand, to help more clearly separate out situations where family unit members or other related businesses may earn commissions in their ain roles not actually continued at all to the CFP® professional's clients and services provided, CFP Lath provides a "safe harbor" exception:

Rubber Harbor for Related Parties. Sales-Related Compensation received by a Related Party is not "in connection with whatsoever Professional Services" if the CFP® professional person or the CFP® professional's Firm adopts and implements policies and procedures reasonably designed to preclude the CFP® professional or the CFP® professional's Firm from recommending that any Client purchase Fiscal Assets from or through, or refer any Clients to, the Related Party.

12) Due Diligence Duties When Recommending, Engaging, And Working With Boosted Persons

One of the key aspects of the CFP® professional's fiduciary Duty of Care to human action with "the care, skill, prudence, and diligence that a prudent professional person would exercise" is the implicit expectation that CFP® certificants only serve in areas in which they have the skills and are capable of providing a professional person level of care in the first place. In other words, where CFP® professionals are not capable of acting with the requisite care and skill (and prudence and diligence), they are expected to not return services, and limit the scope of the Engagement with the Client and/or involve exterior professionals who can render that level of care.

Notwithstanding, CFP® professionals however take both a duty to ensure that when 'boosted persons' are brought into (or referred out from) the client Engagement, that reasonable due diligence has been washed to affirm the quality of the professional existence referred.

Accordingly, under the new rules, CFP® professionals must:

- When engaging or recommending the selection or retentiveness of boosted persons to provide financial or Professional Services for a Client:

- Take a reasonable basis for the recommendation or Appointment based on the person'due south reputation, experience, and qualifications;

- Exercise reasonable care to protect the Customer's interests.

As with other 'principles-based' professional obligations, CFP Board does non explicitly specify what, exactly, CFP® professionals are expected to do in order to satisfy this due diligence requirement when working with outside professionals.

Notably, the Standard requires a CFP® professional to "have a reasonable basis for the recommendation or Date" based on that person'south "reputation, experience, and qualifications", which may include (only doesn't require) going and so far as to actually investigate a related professional person's credentials.

Appropriately, in exercise, the obligation is more than almost the CFP® professional at least determining that the individual has reasonable credibility markers – due east.yard., if they're going to be brought in for complex tax and business consulting, do they have a CPA license and some years of experience doing similar piece of work, or if they're going to conduct a complex insurance assay, do they have advisable professional education and experience. Which, in turn, is part of a broader obligation to "practice reasonable care to protect the Client's interests" – i.east., not refer them to someone who themselves would non be predictable to serve the Client well and/or may take reward of the Client.

Accordingly, while not explicitly required, information technology would be appropriate under this CFP Lath Duty to at to the lowest degree annotation in the advisor's CRM when establishing a new human relationship with an exterior professional what "reputation, experience, and qualifications" are being relied upon as a 'reasonable basis' for recommending or engaging them.

In addition to the upfront obligation regarding the "reasonableness" of engaging or recommending an outside professional, CFP® certificants also accept an ongoing obligation too:

- When working with some other financial or Professional Services provider on behalf of a Client, a CFP® professional must:

- Communicate with the other provider about the scope of their corresponding services and the resource allotment of responsibleness between them; and

- Inform the Client in a timely manner if the CFP® professional has a reasonable conventionalities that the other provider'southward services were not performed in accordance with the telescopic of services to exist provided and the allocation of responsibilities.

In essence, the CFP® professional person, in analogous with outside professionals, is expected to take productive communication about "who does what" and the allocation of responsibleness (e.g., the CFP® professional will assist in discussing the manor planning strategies with the Customer, simply the estate planning attorney will draft the documents for the Customer, while the CFP® professional will have an opportunity to provide feedback on those documents before they go to the Client to help ensure they align to the Customer's goals, and both the CFP® professional person and the estate planning attorney volition be in the final meeting when the Client is ready to sign the documents, etc.).

Furthermore, CFP® professionals are expected to notify the Customer in the event that they discover outside service providers (that the CFP® professional recommended or engaged in the commencement place) are non performing their duties as anticipated. However, fifty-fifty one time the CFP® professional brings in (or recommends out to) an outside political party, they are not necessarily responsible for ongoing monitoring of the exterior relationship. Still, if an issue does come to calorie-free, the CFP® professional has an obligation to inform the Client at that betoken.

Ultimately, the key point is that when a CFP® professional needs to (or under their Duty of Care, has an obligation to) engage in or recommend the Client over to an exterior professional person (eastward.g., a lawyer, accountant, insurance skilful, investment expert, etc.), the CFP® professional is not ultimately responsible for the exterior provider'south work product, just does take an obligation to show a reasonable basis that the private was qualified and capable of doing the work, that the scope of piece of work for the professional person is clear (relative to what the CFP® professional remains responsible for doing), and that if the CFP® professional discovers an issue in the procedure, the Client is informed accordingly.

However, in some cases, the relationship of engaging or referring out to outside professionals is more than 'simply' a professional referral; it may exist an established cross-referral relationship (with an expectation of reciprocation), and/or i in which money exchanges hands (eastward.g., an affiliate or solicitor organisation). In such situations, the CFP® professional person non but has the obligations of determining the upfront reasonableness and ongoing working relationship with outside professionals but too must:

Disembalm to the Client, at the time of the recommendation or prior to the Engagement, any system past which someone who is not the Client will recoup or provide some other material economic benefit to the CFP® professional, the CFP® professional'southward Business firm, or a Related Party for the recommendation or Appointment.

Notably, this disclosure requirement applies "at the time of the recommendation or prior to the Engagement", which means fifty-fifty if the Client is already engaged, a subsequent recommendation/referral that has a remuneration component must withal exist disclosed to them (if it hadn't already been disclosed upfront).

In add-on, the requirement is not only to disclose outright compensation, but someday the CFP® professional (or his/her firm or a related political party) will receive "some other textile economic benefit", which might include an established quid pro quo cross-referral relationship. On the other hand, just "material" economical benefits must be disclosed, which ostensibly would not include informal cross-referrals that may happen or nominal gifts (east.1000., a holiday gift basket received from an attorney or accountant who had received a referral from the CFP® professional, etc.).

thirteen) Comply With The Law

In addition to the fiduciary and other Duties that CFP® professionals have as CFP® professionals, as a (highly!) regulated industry, fiscal advisors are subject field to numerous other regulators as well.

Accordingly, CFP® professionals must also:

Comply with the laws, rules, and regulations governing Professional Services.

Of form, CFP® professionals already have an obligation to comply with the laws and regulations that apply to financial advisors or risk losing their bodily regulatory license to provide such services in the first place. Ultimately, the real point of having an obligation for CFP® professionals to comply with the laws and regulations that may apply to them is that it means a CFP® professional tin can potentially be sanctioned based on violations of the law or other regulators' rules and regulations, even without CFP Lath investigating the matter straight themselves and determining that the fiscal counselor's actions were besides a violation of (other) Duties nether the Lawmaking and Standards. Instead, a finding by the courts or another regulator that the CFP® professional person failed to comply with existing laws, rules, or regulations, is ipso facto a violation unto itself. (Which is important in regulatory matters that pertain to customer privacy, where CFP Board'southward own ability to investigate directly may be limited, and/or equally a matter of expediency to non 're-try' a legal or regulatory affair that has already been tried in courtroom or arbitration.)

In addition, CFP Board'south obligation of CFP® professionals to comply with the constabulary applies not only to their direct activities merely also to activities that may consequence in misconduct in which they are complicit with other (CFP® professionals or non-CFP) individuals, stating:

A CFP® professional may not intentionally or recklessly participate or help in some other person's violation of these Standards or the laws, rules, or regulations governing Professional person Services.

On the other hand, it's notable that the obligation to "Comply With the Law" – to the signal that failing to do so is itself a violation of the Code and Standards– pertains only to the laws "governing Professional person Services". However, violations of other laws (eastward.g., drunk driving) that practise not pertain to the fiscal services industry, and the advisor's delivery of Professional Services, may nonetheless exist in violation of the Duty Owed to CFP Board to Refrain From Adverse Comport.

fourteen) Duties When Selecting, Using, And Recommending Applied science

In the past, rendering professional person services was primarily about the professional themselves rendering services according to their Duty of Care to human activity with "the care, skill, prudence, and diligence that a prudent professional person would do". In essence, to only provide communication in areas in which they have sufficient expertise and experience to propose.

All the same, in an increasingly technology-driven world, the reality is that fiscal advisors increasingly rely upon the technology they utilize to conduct noun analyses of customer needs in order to craft recommendations. Accordingly, as technology is becoming an extension of the financial counselor, the CFP® professional's due diligence obligation at present extends to their selection of applied science to use with clients:

A CFP® professional must exercise reasonable intendance and judgment when selecting, using, or recommending any software, digital communication tool, or other engineering while providing Professional Services to a Client.

Notably, the obligation of CFP® professionals to appraise their technology goes across merely having a "reasonable footing" to believe that the software is appropriate, but that they actually "exercise reasonable intendance and judgment" when selecting, using, or recommending software.

Of course, the reality is that as licensed individuals (east.g., by FINRA, the SEC, or a state insurance section), regulators generally already impose non-trivial requirements on financial advisors in various channels to conduct advisable due diligence on their applied science, particularly from the perspective of cybersecurity and maintaining the integrity of client data and customer privacy.

Appropriately, the due diligence on engineering vendors conducted past broker-dealer and similar platforms would likely already suffice in coming together the reasonable care requirement for CFP® professionals (assuming they practice at to the lowest degree verify that their platform did such due diligence themselves), and to the extent an RIA is conducting its due diligence of a vendor's cybersecurity practices with respect to non-public information of clients, such reviews may satisfy the obligation under CFP Lath'southward Code and Standards as well. (Though notably, those providing financial advice services every bit non-registered individuals – due east.g., 'fiscal coaches' – may demand to take additional steps to ensure they are meeting this technology vendor due diligence requirement.)

On the other hand, the obligation of CFP® professionals to be diligent when selecting technology goes across 'just' the option of the platform and its functionality (and protections for private client data):

A CFP® professional must have a reasonable level of understanding of the assumptions and outcomes of the applied science employed.

In other words, proper selection and due diligence of advisor technology become beyond but its cybersecurity and core features. Ultimately, to the extent that the software facilitates advice in particular – for instance, fiscal planning software used to craft recommendations, various "robo-advice" tools that assemble and match client input to recommended portfolios, etc. – the financial advisor must actually have a 'reasonable' level of understanding of how the software arrives at the recommendations it makes (i.e., the assumptions it uses and how those lead to the outcomes it provides).

Notably, though, CFP® professionals are not necessarily expected to independently audit and verify the calculations of the software itself (across, as noted earlier, having exercised reasonable care and judgment in selecting a credible vendor in the first place). Still, CFP® professionals cannot necessarily treat financial planning or robo software as a 'blackness box' where data goes in, and output comes out, without an agreement of the assumptions and machinations the software uses behind the scenes to come up to its conclusions and recommendations. Which, notably, may put additional pressure on some software vendors in the coming years to explicate more than explicitly how, exactly, their recommendation engines work (so that CFP® professionals can have the necessary understanding to comply with their Duty to understand their Technology).

Similarly, CFP® professionals must also take steps to ensure that the output of the software is consistent with what it purports and is intended to analyze and recommend:

A CFP® professional must take a reasonable basis for believing that the technology produces reliable, objective, and appropriate outcomes.

Once again, CFP® professionals are not necessarily required to deconstruct or fully audit their technology, but must have some 'reasonable basis' that their technology produces reliable, objective, and appropriate outcomes. Potential approaches may include:

- Input some 'typical' client scenarios and evaluate the output/outcomes to decide if they are equally expected;

- Compare the software output (e.g., as a user or via a demo) to output/results from other established software tools;

- Evaluate the credibility of the software provider, its experience and squad, and the expertise it hired or called upon to pattern the software; and

- Examine any third-political party expert or user reviews of the software for feedback.

Notably, CFP® professionals are expected not only to evaluate the reliability and appropriateness of their software output, just also the objectivity of the output. Accordingly, CFP® professionals should also inquire of their software companies whether they receive any material acquirement outside of their User Fees for the software itself – an increasingly common approach as more financial planning and wealth direction software companies may employ their software to facilitate the sale of investment or insurance/annuity products that could potentially compromise their objectivity.

Of course, as with CFP® professionals themselves, the presence of a conflict of interest does not automatically hateful that results/outcomes have been tainted; even so, the "Applied science Duties" of CFP® professionals do at least impose on them an obligation to empathize whether such conflicts of interest may be present with their technology providers, and if so to accept a reasonable basis for assertive that the software company is maintaining the objectivity of its output (i.eastward., what are the software company's policies and procedures to mitigate its ain conflict of interest?). And if the CFP® professional's evaluation of their software is that its results and recommendations would not be objective, the CFP® professional has an obligation and Duty non to utilise the software.

xv) Not Borrowing From, Lending To, Or Commingling Fiscal Assets With Clients

For centuries and even millennia, it has been recognized that when 1 person is entrusted to care for the financial and business concern affairs of some other, the trustee should not manage those assets in his/her ain interests, but instead should manage those avails in the interests of their beneficial owner… which, over time, evolved into the fiduciary "best interests" Standard of today.

Notably, though, the thought of managing the financial affairs of the Client in the "best interests" of that Client isn't necessarily or even primarily about finding the i 'all-time' solution for the Client. Instead, it'due south about recognizing that the counselor has an obligation to manage affairs and brand recommendations, non in a manner that benefits their own interests and their Client's, but one that benefits only (i.e., is best for) their Client.

In other words, the origins of the "all-time interests" Standard are primarily about not self-dealing a client'south financial assets and diplomacy for ane'due south ain benefits. For instance, being responsible for client assets just using them for the advisor or trustee'due south ain business interests (i.e., borrowing money from a client, or lending a customer's coin to the advisor or trustee) could potentially put the advisor'southward interests at a crossroads against the Client's, and therefore brand it incommunicable for the advisor to go along to manage the client'due south assets in their own best interests.

For case, if the advisor'south business organisation was declining afterward borrowing money from the Client, there would be an undue temptation to infringe more from the Client, rather than telling them to cut their losses at the hazard of further impairing the advisor's business interests. Similarly, if the advisor had loaned money to the Customer, it would be hard to give a recommendation to the Client to default, fifty-fifty if that was the most advisable class of activeness.

Accordingly, ane of the longest standing obligations of fiscal advisors and fiduciaries (and trustees in general) is not to borrow from, lend money to, or commingle financial assets with clients, due to the potentially untenable conflicts that such actions can create (rendering it incommunicable in agin situations for the advisor to objectively provide recommendations to the Client).

In the context of the Duties that CFP® professionals accept to their clients, CFP Board'south Lawmaking and Standards similarly stipulate that:

- A CFP® professional may not, direct or indirectly, borrow money from or lend money to a Client unless:

- The Client is a member of the CFP® professional's Family; or

- The lender is a business concern organization or legal entity in the business organisation of lending money.

- A CFP® professional may not commingle a Client's Financial Assets with the Fiscal Assets of the CFP® professional or the CFP® professional's Firm.

Notably, CFP Lath does provide an exception for financial advisors to borrow or lend coin to family unit members who are clients, recognizing the practical realities that sometimes family unit members exercise infringe and lend within the family. (And in the cases of affluent families, may even be washed intentionally as intra-family unit loans for manor planning purposes.)

However, outside of family unit members who are Clients, CFP® professionals are strictly prohibited from borrowing money from or lending money to clients, unless that Customer happens to be a business organization or entity otherwise already in the business of lending money (e.thou., in the case of an advisor who manages a 401(k) plan for a depository financial institution that is a bona fide lending institution so separately wants to take out a business loan from that bank).

On the other paw, when it comes to the commingling of assets with Clients, CFP Board's Code and Standards outright prohibits commingling in all scenarios. Which means in situations where even family members are Clients of the CFP® professional person or his/her firm, assets must be separated, potentially creating challenges in the case of the CFP® professional person managing a family trust in which he/she is also a beneficiary. (Though if the family trust didn't compensate the CFP® professional, ostensibly the trust would no longer be a "Client" and thus not run afoul of the rules.)

In the cease, the cadre requirement of CFP® professionals – as with any professional person – is to act in the best interests of their clients and adhere to the Code and Standards expected of whatsoever professional. Which can and do apply across all of the professional person'south activities, from the advice they provide to clients to how they conduct their own business organization diplomacy. For which CFP Board prescribes a series of 15 Duties Owed To Clients to guide CFP® professionals on what it really takes to meet their professional person fiduciary obligation to clients.

In this context, CFP Board'due south Lawmaking and Standards are not meant to be an onerous series of new or different duties, and in practice are often ones that about professionals adhere to anyhow, if only for expert concern practices. Nonetheless, by establishing formal Standards of Conduct, CFP Lath also implicitly reserves the correct to discipline CFP® professionals who fail to adhere to the requirements… or in the extreme, to revoke the CFP® marks altogether from those who neglect to represent themselves properly as professionals!

What Requirements Do Service Providers Owe To Their Client,

Source: https://www.kitces.com/blog/the-15-fiduciary-duties-to-clients-that-cfp-professionals-must-comply-with/

Posted by: wentworthlinet1989.blogspot.com

0 Response to "What Requirements Do Service Providers Owe To Their Client"

Post a Comment